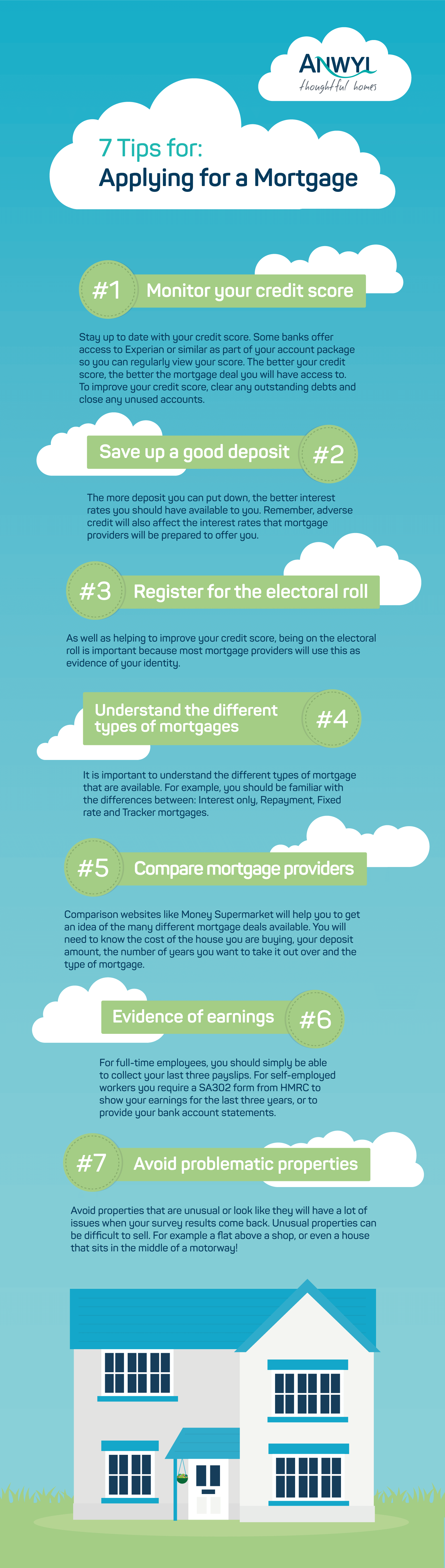

Applying for a mortgage is rarely straightforward, so in order to make sure it goes as smoothly as possible, these tips will help!

When you find your ideal home, you want to make sure that nothing prevents you from buying it. You will face some challenges, such as selling your old home if you have one but one of the biggest barriers of signing on that dotted line is your mortgage application. Applying for a mortgage is rarely straightforward, so in order to make sure it goes as smoothly as possible, these tips will help:

Monitor your credit score

Leading up to your application, stay up to date with your credit score. Some banks offer access to Experian or similar as part of your account package so you can regularly view your score. Alternatively, you can pay to get a report. You will be able to check if there have been any missed payments or any other adverse credit history in your credit score and reports. The better your credit score, the better the mortgage deal you will have access to. To improve your credit score, clear any outstanding debts and close any unused accounts. It can take time to rebuild your credit score after problems, so always check your score before you submit an application as a declined application can further damage your credit score.

Save up a good deposit

In the current mortgage market, the only way you are likely to get a mortgage without a deposit is if you have a guarantor that puts their own property or money at risk, in the event that you miss payments. Otherwise, like most applicants, you will need to save a good deposit to put down against the mortgage. The more deposit you can put down (as a percentage of property value), the better interest rates you should have available to you. Remember, adverse credit (see tip 1) will also affect the interest rates that mortgage providers will be prepared to offer you.

Register for the electoral roll

As well as helping to improve your credit score, being on the electoral roll is important because most mortgage providers will use this as evidence of your identity. So make sure that your details are fully up to date before you apply for a mortgage.

Understand the different types of mortgage

Before you start the application process, it is important to understand the different types of mortgage that are available. For example, you should be familiar with the differences between:

Interest only

Repayment

Fixed rate

Tracker

Compare the different mortgage providers

Comparison tables provided by websites like Money Supermarket will help you to get an idea of the many different mortgage deals available. To get an accurate calculation, you will need to know the cost of the house you are buying, your deposit amount, the number of years you want to take it out over and the type of mortgage. This will then calculate your Loan to Value, which is they key figure that decides on which deal you can apply for. You can also see the different fees and other details such as early repayment charges for each different mortgage deal. It is worth checking if you get a better deal going direct with the mortgage provider rather than through the comparison site.

Evidence of earnings

For full-time employees, you should simply be able to collect your last three payslips. For self-employed workers, it can be a lot more difficult to provide evidence, as you require a SA302 form from HMRC to show your earnings for the last three years, or to provide your bank account statements. You will also be required to supply a recent letter from a utility company or your bank that provides evidence of your address.

Avoid problematic properties

If you want to be in your new home as quickly as possible then avoid properties that are unusual or look like they will have a lot of issues when your survey results come back. Unusual properties can be difficult to sell. For example a flat above a shop, or even a house that sits in the middle of a motorway! Mortgage lenders are usually reluctant to lend money on properties deemed more risky for selling on. Lots of older properties are likely to bring up a few issues with the survey and you can simply use them to negotiate on the house price but if the seller prefers to get the work done themselves then it could really hold you up.

Applying for a mortgage is rarely straightforward, so in order to make sure it goes as smoothly as possible, these tips will help!

When you find your ideal home, you want to make sure that nothing prevents you from buying it. You will face some challenges, such as selling your old home if you have one but one of the biggest barriers of signing on that dotted line is your mortgage application. Applying for a mortgage is rarely straightforward, so in order to make sure it goes as smoothly as possible, these tips will help:

Applying for a mortgage is rarely straightforward, so in order to make sure it goes as smoothly as possible, these tips will help!

When you find your ideal home, you want to make sure that nothing prevents you from buying it. You will face some challenges, such as selling your old home if you have one but one of the biggest barriers of signing on that dotted line is your mortgage application. Applying for a mortgage is rarely straightforward, so in order to make sure it goes as smoothly as possible, these tips will help: